AI disclosure statement:

Zahra Mirkelam says investing was a foreign concept to her until she graduated university.

“I didn’t even think about investing until I was 20,” says Mirkelam, a Ryerson alumna who now works at BMO. “And that’s because no one ever showed me what it was or how to begin.”

Mirkelam taught herself the basics of investing through YouTube videos and other online resources, but says it’s still difficult for her to fully wrap her head around.

“You don’t really learn about investing unless you have parents who are wealthy enough to invest themselves, which most people don’t. It’s a great way to make passive income that many people don’t know anything about.”

Getting started with investing at any age can be a daunting and confusing task. Education on the topic is typically optional in school and almost overwhelming online.

In a world where saving for a car, house or even retirement is getting further out of reach every day, investing skills can seem almost unattainable to the average Canadian. Yet economists and financial planners point to investing as the answer to reaching your long-term goals.

So, what does it mean?

Forbes defines investing as buying an asset at a low price and selling it at a higher price. Seems simple, but assets can look like anything; from stocks to bonds to commodities, and even real estate. If this sounds complicated to you, don’t worry, you’re not alone.

According to a press release from BMO, even though Canadians are investing, only one-third believe they understand the ins and outs of it. In addition, 67 per cent of Canadians are unable to identify the differences between a Registered Retirement Savings Plan, or RRSP — which is a vehicle for saving for retirement, and a Tax-Free Savings Account, or TFSA, — which is used for any type of savings goal. If this sounds like you, then you’ve definitely not alone when it comes to financial literacy.

When it comes to getting started, Daniel Tut, assistant professor of finance at the Ted Rogers School of Management, says the best thing beginners with a low income can do is take a personal finance course.

“Whether that be in high school or at a university level, it’s best to be educated on the basics of money management before diving into the world of investing.”

Tut recommends high school students look into any business or math courses that talk about money, while university students should consider taking at least one finance course as an elective.

Lu Zhang, assistant professor of finance at the Ted Rogers School of Management, agrees with taking personal finance courses, but also stresses the importance of keeping your account as debt-free as possible while you’re in and out of school.

“First step would be to pay off any high-interest debt as soon as possible before investing,” she says. “This includes student loans or any credit card debt. That way, any profit you make in the market isn’t eclipsed by the interest you’re being charged on debt you have.”

But whether you have debt to pay off or money to invest, Tut says the best place to turn for financial advice is your bank.

“Seems logical, right?” Tut says. “Making an appointment with a free financial adviser at your bank can be really helpful. They know the ins and outs of the market and can help you get started.”

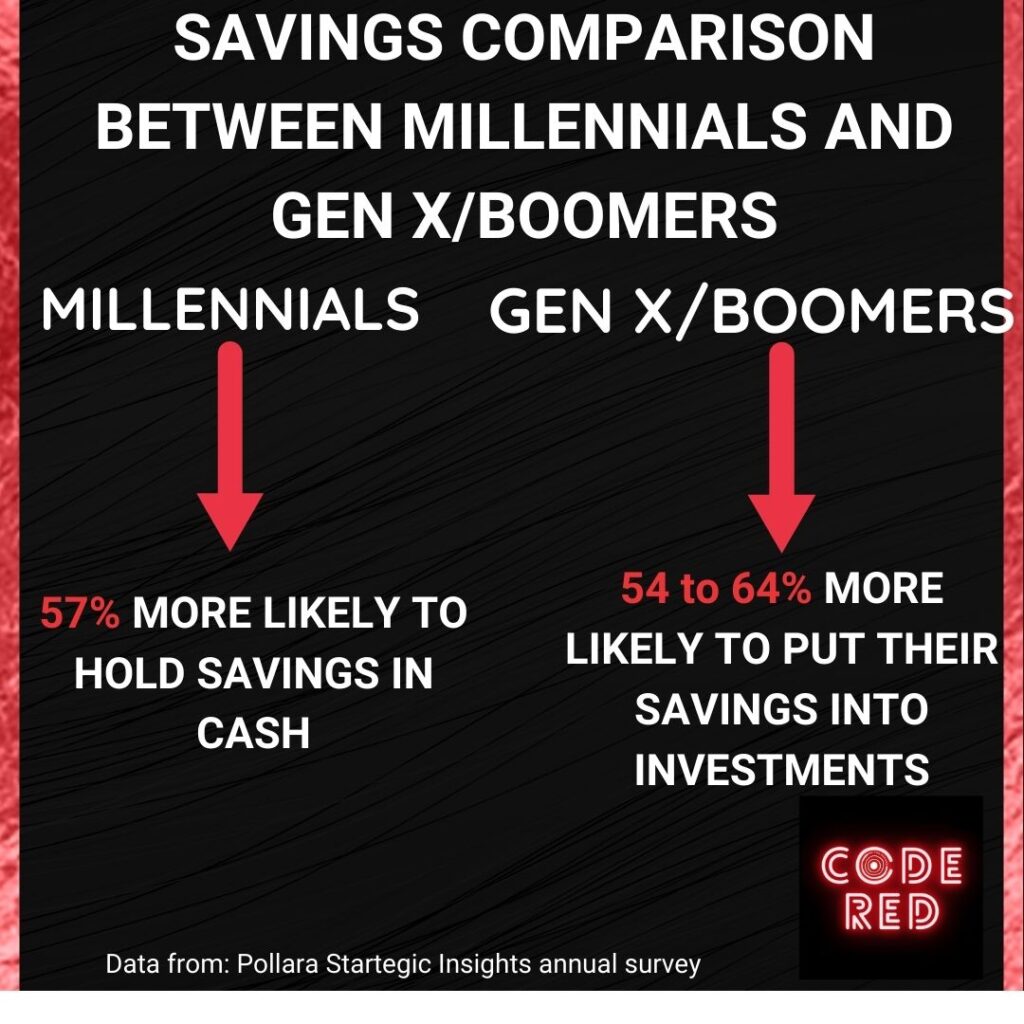

Having that resource available doesn’t necessarily mean many people will use it. According to an annual survey conducted by Pollara Strategic Insights, more than half of millennials hold their cash in savings rather than investments.

Zhang says that when it comes to investing, proceeding with some caution around your hard-earned money is not only healthy, but actually smart.

“I think it’s fair for people to be scared of investing after the recent crash we had in 2020, but if you’re investing for the long term over many years, those recessions won’t matter as much.”

Investing in the long term is the way to go, according to Zhang. Young people are in a great spot when it comes to accumulating wealth because of a simple concept called compound interest.

Claudia Latino/On The Record

“This means if you are saving or borrowing, you’re not only accumulating interest on the amount you borrow or invest but also on the interest you accumulated in the previous period.” That’s why it’s important to pay off any loans before attempting to make your money work for you.

Tut emphasized the importance of compound interest when investing at an early age, saying it’s your biggest earner when it comes to growing your savings.

“Think of it like learning new technology,” he says. “The younger you are, the easier it comes to you while your parents struggle to get it. It’s the same with investing.”

If investing is starting to sound intriguing but still a little intimidating, Zhang points out that you don’t need the stress of the stock exchange to grow your wealth.

“Some of the most beginner-friendly investments you can make today are mutual funds and ETFs (exchange traded funds),” Zhang says. “They pool money together and spread them out over hundreds of different companies, so your risk is minimized but the return is consistent.”

If minimizing risk at the expense of larger returns doesn’t sound like your goal, it doesn’t have to be. The good news, Tut says, is that there’s a place in the market for everyone.

“There’s three types of investors. Risk seekers, risk-averse, and those in the middle,” he says. Risk seekers typically go for more volatile investments that can yield higher returns, like cryptocurrency and individual stocks. Those that are more averse to risk stick with index funds, mutual funds, bonds and ETFs which, through the ups and downs of the market, tend to trend upwards over time.

“Those that are neutral usually have lots of wealth to spread out,” Tut says, “keeping some safe from risk while gambling with the rest to maximize returns.”

The type of investor you are will largely depend on the amount of money you have to put into the market and the amount of time you want to keep it there.

“If you have more time, you might take more risks than someone that needs to slowly grow their wealth for the next few years.” But the only way to know that is to pick a goal and a timeframe before you start.

Mirkelam agreed that even though starting earlier would’ve yielded her better results, she’s happy she started at all. “I’m glad we have the online resources we do today so we can learn concepts that should’ve been taught in schools in the first place.”

Investing can seem like a foreign and scary concept, especially when your life savings are on the line, but it doesn’t have to be. No matter how many zeros you have in your bank account, any amount of money can be grown using the power of smart financial planning, compound interest and — your best asset — time.